With Hurricane Irene barreling through the Bahamas as a strong Category 3 storm, the Eastern seaboard of the United States watches with trepidation and prepares to brace for what could be the strongest and most damaging hurricane to hit the East Coast in decades. All hurricane and storm tracking agencies are now concurring that the projected path of Irene will most likely make initial contact with the U.S. mainland in the Hatteras/Outer Banks areas–two hot-spots of the North Carolina tourism industry. Mandatory evacuations have been ordered for visitors to the Outer Banks islands and may be extended to residents as Irene’s progress is tracked. Even more ominous is the path expected beyond the Carolina coast. Hurricane Irene is expected to continue a north-northeastern track, clinging to the Eastern coastline while delivering hurricane-force winds and flooding rains to major metropolitan areas such as Washington, DC, Pennsylvania, Delaware, New York, Rhode Island, and Massachusetts, and continuing to the Canadian border. The projections of this storm place a population of approximately 55 million people at risk for potentially life-threatening conditions.

Hurricanes have become a large part of summer’s end for those living in the Southeast and, in some cases, have had a devastating economic impact on the areas in their path. The related costs are in the billions of dollars and the burden is felt by virtually everyone — industry, federal and state governments, businesses, and homeowners. For instance, the City of New Orleans has a 7-million dollar contract in place which would ensure bus transportation for residents to a safe location in the event they are again threatened with a storm such as Hurricane Katrina. The city of New Orleans’ cost of recovery, and implementation of safety measures in the event of another destructive storm, is in excess of $100 billion dollars and counting.

According to global weather studies, we are now in an era in which more, rather than fewer, of these severe weather events can be expected. My fifteen years in the insurance restoration industry, both as a contractor and as an expert/appraiser for insurers & owners, has enabled me to identify the critical elements of the recovery and claims process. These steps are detailed below.

Documentation — Immediately following a loss, safety concerns should be the first item of attention. Once safety issues have been identified and dealt with, an immediate plan for the mitigation of the loss should be developed. It is also at this early stage that the documentation of the conditions should be completed. Before the first tree is cut away from the building or the first temporary roof is applied, the property should be photographed in its entirety. It is wise to also consider a photo of your property within the context of the neighborhood to establish that surrounding properties are equally affected. It is important to include landmarks in your photo, along with pictures with a greater perspective, as well as close-up shots of the property — all with the date stamp on the photo. The pictures should include the flood line if one exists — this would include a visible tape measure marking the height of the floodwaters from the finished floor elevation. Objects that impacted the structure or remain on the building should be photographed before they are removed unless they create an ingress/egress safety hazard. The ability to take digital photos will greatly improve your ability to share data with insurers and others. Remember: Never submit your original photos to involved parties!!! Keep originals in a safe place, while submitting copies to insurers and others. It is imperative to photograph the building and its contents PRE-STORM (prior to the loss) in order to prove the original condition of your property, especially in the case of a total loss or complete loss, as was all too common after Hurricane Katrina on the Gulf Coast in 2005.

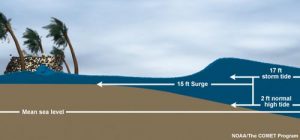

Causation, Quantification and Costs — The next step in the restoration of a property affected by an insured loss is to establish how the damage occurred, what was the result to the structure, and what will it cost to restore the property. This is where the restoration can become very complicated and prompt an individual to consult with an expert in the industry. In the case of wind vs. flood, there are many, many factors – more than could be enumerated in this report; however, it is critical to develop an understandable chain of logical conclusions. One would need to examine the flood line, the impact of objects carried in the flood (either still or velocity water), the elevation of the property, the wind speeds, and the presence or absence of straight line or tornado winds. Each of these factors would then be compared to the structure and its attributes. Once an opinion is reached as to the cause of damage, the loss can then be broken down according to the peril and the actual size and type of building materials affected. At this point, it would be prudent to locate your house plans and enlist the services of a professional to complete an assessment of damages or conduct such an assessment oneself. This assessment should include the stated value of each affected item with each item delineated by cause; for example, the roof may be 9,000 square feet of EPDM with 1.5 inches of ISO-insulation below OR the flood may have taken the bottom four feet of drywall on the bottom floor. Having a trusted contractor, engineer, architect, appraiser, or expert available to break out and apply costs to this data will greatly enhance your ability to have an “apples to apples” comparison with the numbers established by the adjuster. There are many programs that specialize in this type of cost estimating. My personal preference is Xactimate software, having utilized it for more than a decade. Xactimate, and similar software programs, compile costs for individual areas and provide them to insurance professionals and restorers, and provide line-by-line details of the damages in reference. While they may appear daunting, once one is familiar with their operation, a great amount of detail can be documented and calculated quite easily.

Mitigation — The second step is to mitigate (to make less severe) the damages, as required in most insurance policies. Following a major hurricane, it may be some time before you will be visited by your insurer. At this stage, it is the homeowner’s financial responsibility to mitigate the loss and prevent the loss from becoming worse, if possible. In addition to preventing further entry of water, the implementation of a plan to remove water-damaged building components is necessary. As many people are aware, the presence of mold is potentially harmful to one’s general health, and can even be toxic to certain people. According to research from many sources, mold can begin in 24–48 hours after the introduction of water to cellulose building components, i.e., drywall, interior wood trim, wallpaper, etc. (EPA Mold Guide). Often, people are not even able to return to their properties in this time frame, particularly on the barrier islands. Many insurance policies specifically exclude the costs associated with detailed mold remediation work; therefore, it is advantageous to remove water-damaged building components promptly and treat the affected areas with a mildewcide to prevent the spreading of mold.

In addition to the direct physical damages and costs, there may be requirements associated with law and ordinance for particular areas in regard to flood and wind speed zones. If you live in a flood zone, do not be surprised to learn that your property may require elevation after a loss – especially a loss determined to be more than 50% of the value of the structure (pre-storm). In some cases, this is not practical and relegates the property to that of a total loss requiring demolition and reconstruction compliance.

Important Links:

Complete General Contractors, Inc. specializes in hurricane damage restoration from residential, commercial, industrial and by municipality. John Minor has worked post-hurricane sites since Opal in 1995; his experience is far-reaching – from the Carolina’s to Texas and all along the coast of Florida. The staff of Complete can meet with you to review your preparedness plan, and we will be there afterward should you ever need us. We specialize in the actual restoration, prevention, as well as, dispute resolution of a claim. Call the company the pros choose – call Complete.

This information should not be substituted for professional legal advice; consult with your lawyer for legal advice and ask your insurance professional to discuss the details of your policy and insurance needs.