Appraisal has been around at least since 1888 in Scottish Union & National Insurance Company v Clancy but remains a lesser-known method of resolving property insurance claims arising from wind, water, fire, or other insured losses. Appraisal is defined as the determination of what constitutes a fair price, valuation or in the policy – the amount of the loss. While appraisal is included in the majority of policies it has different forms and interpretations depending on to whom one is speaking.

Some companies have simply written it out of the policy for one reason or another. Others have made participation in the appraisal process something that both sides of the contract must approve. Fortunately, other insurance companies see it as a viable way to resolve claims in an alternative dispute resolution program. Many large and small claims get successfully resolved in the appraisal process every day without pointless litigation. This is not to say that appraisal is correct for every claim as appraisal is not a place for coverage or policy disputes.

Appraisal has proven that it can serve the purpose of resolving wind, flood and fire claims with fresh eyes on a subject without a preconceived interest. It can also remove the personal feelings that can arise among insurance representatives and property owners. In the appraisal of a claim we try to step back from the issues of the day and understand the value of the loss.

In today’s practice one party or the other will:

Demand or Invoke the Appraisal Clause. At that time, one should read their policy and specifically the Appraisal Provision. Essentially the Demand is just that “I demand appraisal” list the coverage and name the appraiser.

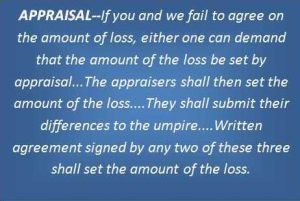

The Appraisal Process

“If you and we disagree…” While the language seems simple enough there are meanings based on the wording. It requires a number of things:

Competency – Required by each appraiser, which seems simple enough. Competency is obviously a subjective word but, in my experience, I usually find good appraisers are not always consistent or compliant but usually competent.

Disinterested – This may or may not be required depending on the words of the policy and jurisdiction. It is usually interpreted to mean not being paid a % of the loss and strictly paid by the hour. The hourly rate can range from maybe $125.00 per hour to more than $500 an hour on a complex commercial or industrial loss.

Umpire Agreement – The policy typically then calls for the agreement on an insurance claims umpire to decide any differences between the parties. Many believe this agreement to the umpire should be done as soon as the appraisal is invoked and commenced by the appraisers or counsel. The fire, wind, homeowners or commercial policy generally gives a time that either side, if they cannot agree on an umpire(s) to go to the court having jurisdiction and petition for an umpire.

Usually I select an umpire first thing but if you feel the opposing appraiser is going to be reasonable or the opposing appraisers’ reputation in the industry suggests same you might try to postpone selection. Now, not getting an umpire and moving forward can also backfire. After you move forward in an appraisal and are apart the selection of the umpire after the disagreement is much more difficult and almost certainly requiring court appointment.

The next question is court appointment. Many appraisals are running parallel with the surrounding litigation and the umpire comes from that process packaged with the appraisal. Most feel that both sides should get a shot at presenting their umpire suggestions. But beware of Umpire Appointment by “Either May” While I agree that the panel should work together, I do not see it detailed that way in the test of the document the four corners of the appraisal language. It just says that either may petition the court. This has left me on one occasion a unilateral appointed umpire not of my selection.

It just says either may… I will leave that one for you figure out. I will assure you of one thing if I believe the other appraiser is headed to the courthouse to get an umpire on day 20 you will see either my white truck in the courthouse parking lot or that of counsel. The worst thing is to get a bad umpire and you will know it when it happens.

Appraisal Process – The process of the appraisal should be simple but leave it to very smart people to make an agreement of 2 out of the 3 difficult. The process requires both appraisers separately setting the “value of the loss”. In some states the appraisers have more latitude to determine the scope where in others it is more controlled. In the flood appraisal provision of the NFIP policy the scope is set before the appraisal commences.

After scope is decided or agreed to be different both sides separately state the “value of the loss”.

If the two appraisers cannot agree then the differences alone should be taken to the umpire for resolution. It is my opinion that the umpire can then either side with one or the other by item or come up with their own number based on agreement to part of each side’s argument. I do not believe it is one way or the other – period.

Appraisal Award – An appraisal requires signature of two of the three appraisers to be an award. In some occasions the process of the appraisal gathers agreement of the three parties of the panel and becomes a three-party award. In general, the award needs to include the parties to the contract, the claim number, date of loss, and type of loss.

The award should be broken out by coverage with each value depreciated as applicable and may be backed up by an estimate or appraisal of the damages. The award should have enough detail that any reader would be able to understand the damages contemplated under the award. This is especially important in replacement cost policies as a good award can allow for easy application and handling of recoverable depreciation requests.

Appraisal is a great process that allows disputed property claims to get resolved. Our group has worked as appraisers on more than 1,000 property claims over the last 20 years in a dozen states.I have been the federal court appointed umpire on 10-million-dollar fire claim and the insurance company appraiser for the wind carrier after Hurricane Katrina. We have resolved 25 million dollar losses for property owners in appraisal and after 20 years and all of that, it all comes down to reasonableness and veracity of opinion. Call it like you see it, keep your mind open just in case you are not right, be just, and be kind.