Appraisal Provision in Homeowners & Commercial Policies

Appraisal has been around at least since 1888 in Scottish Union & National Insurance Company v Clancy but remains a lesser-known method of resolving property insurance claims arising from wind, water, fire, or other insured losses. Appraisal is defined as the determination of what constitutes a fair price, valuation or estimations of worth or in the policy the amount of the loss. While appraisal is included in the majority of policies it has different forms and interpretations depending on to whom one is speaking. Some companies have simply written it out of the policy for one reason or another. Others have made participation in the appraisal process mandatory only if it is a unilateral decision. Yet other insurance companies see it as a viable way to resolve claims in an alternative dispute resolution program. Appraisal has proven that it can serve the purpose of fresh eyes on a subject with appraisers without a vested interest. It can also remove the personal feelings that can arise among insurance representatives and property owners.

In today’s practice, one party or the other will Demand or Invoke the Appraisal Clause. At that time one should read their policy and look at the wording of the policy very carefully

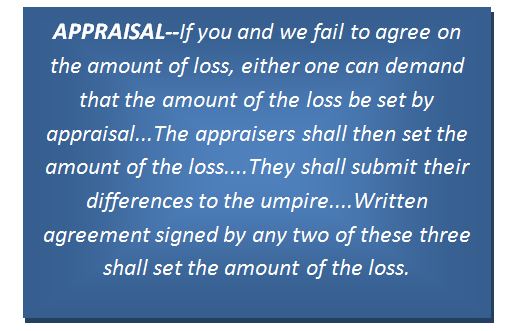

Typical Appraisal Language

The following is standard language but it may vary from state to state:

While the language seems simple enough there are hidden meanings based on the wording. It requires a numbers of things including competency by each appraiser, which seems simple enough. Competency is obviously a subjective word but in my experience I usually find competent appraisers not always consistent or compliant but usually competent. In some states it requires the appraisers to be disinterested this is usually interpreted to mean not being paid a % of the loss and strictly paid by the hour. The hourly rate can range from maybe $125.00 per hour to more than $500 an hour on a complex commercial, or industrial loss. The policy typically then calls for the agreement of an umpire to decide any differences between the parties. Many believe this agreement to the umpire should be done as soon as the appraisal is invoked and commenced. The fire, wind, homeowners or commercial policy generally gives a time that either side, if they do not agree, with the proposed umpire(s) of the opposing party can go to the court having jurisdiction and petition the court for same. There are two wrinkles in this, the first being do the appraisers even have to select an umpire. Can the just not disagree not set an umpire and go kick bricks at the site and see if the two can work it out? My answer to that question would likely be yes if you feel the opposing appraiser is going to be reasonable or the opposing appraisers’ reputation in the industry suggests same. Now not getting an umpire and moving forward can also back fire and make the selection of the umpire after the disagreement much more difficult and almost certainly requiring court appointment.

The next question is court appointment. Many appraisals are running parallel with the surrounding litigation and most feel that if the court is going to be involved then both sides should get a shot at presenting their umpire suggestions. While I agree that the panel should work together I do not see it detailed that way in the test of the document the four corners of the appraisal language. It just says either may… I will leave that one for you figure out. I will assure you of one thing if I believe the other appraisers are headed to the courthouse to get an umpire on day 20 you will see either my white truck in the courthouse parking lot or that of counsels. The worst thing is to get a bad umpire and you will know it when it happens.

The process of the appraisal should be simple but leave it to very smart people to make and agreement of 2 out of the 3 difficult. The process should include both appraisers separately stating their values. In some states, the appraisers have more latitude to determine the scope where in others it is more controlled by the process thus far and venturing away from the scope is frowned on and in some situations a reason for a side to contest an appraisal outcome. After scope is decided or agreed to be different both sides separately state the “value of the loss”. If the two appraisers cannot agree then the differences alone should be taken to the umpire for resolution. It is my opinion that the umpire can then either side with one or the other by item or come up with their own number based on an agreement to part of each side’s argument. I do not believe it is one way or the other period. Some umpires disagree with me and that certainly gives plenty of reason to act fairly when presenting your positions.